The GBP/USD extended its decline a little below the 1.28 area by Tuesday mid-morning European trade, after falling on Monday, states Fawad Razaqzada of Trading Candles.

Since Friday, the cable hasn’t moved much, holding in a tight range. But we are expecting volatility to increase ahead of key events taking place this week, starting with some manufacturing PMI data out of the US. As well as some more top-tier US data in the next few days, we also have the Bank of England’s rate decision to look forward to. For now, I am expecting moderate further downside for the GBP/USD, owing to the dollar’s overall positive trend.

Dollar Resumes Higher

There was a bit of uncertainty about whether the dollar would push higher on Monday. But after its initial weakness, it did find support and rose modestly against a basket of foreign currencies, with the Japanese yen leading the declines among the major currencies after the BoJ offset the impact of its yield curve control policy change by conducting additional purchase operations to cap the rise in JGB yields. Overnight saw the Australian dollar sink further lower after the RBA decided against a rate hike. This also aided the dollar’s recovery. So, there’s certainly a risk the greenback could gain more ground ahead of a busy week after the dollar index closed higher for the second consecutive time in as many weeks.

The greenback has found renewed strength in recent days thanks to data highlighting the resilience of the world’s largest economy, where signs of disinflation have been offset by strength in consumption, suggesting that a severe recession can be avoided, even with interest rates at 5.5%—the joint highest with New Zealand among the developed economies.

In the eyes of the Fed, monetary policy is quite restrictive now, and further rate increases might be avoided. But with the world’s largest economy holding its own relatively well, this means monetary policy may remain restrictive for longer than perhaps some other important economic regions around the world.

There are about two months until the Fed meets again, which means a lot can change in the interim in terms of data. Inflation is obviously in focus. But the Fed will also keep an eye on other macro indicators in determining whether to hike further.

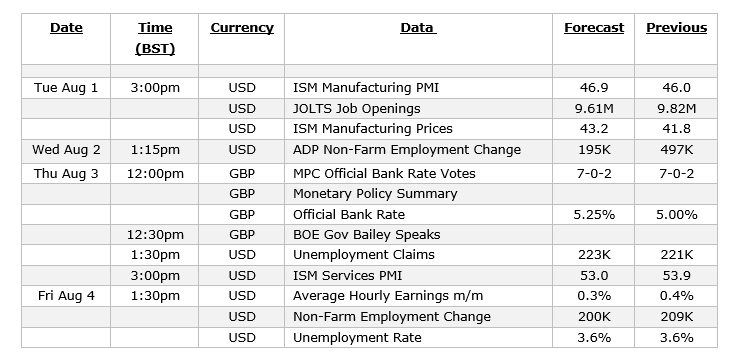

Key Data to Watch for the Cable

The ISM manufacturing PMI data will kick off a busy week for US economic calendar this week. Here are the main data highlights to watch if you are trading the GBP/USD:

The manufacturing sector has been weak across the world in recent months, especially in Europe. The US ISM manufacturing PMI was last in the positive territory in November. Since then, the sector has been in contraction territory (below 50.0) with activity deteriorating continually. The last reading of 46.0 was the lowest since June 2020, at the height of the pandemic. This time, the PMI is expected to show a modest improvement (to 46.9).

Looking ahead to the rest of the week for US data, we will have the ADP private sector payrolls report on Wednesday, followed by the ISM services PMI on Thursday, and then—the big one—the official nonfarm payrolls report on Friday.

The dollar’s bullish momentum faded somewhat on Friday, though, after the Fed’s favorite inflation measure—core PCE—came in a touch softer, although this was offset by a stronger-than-expected personal spending print, which was up 0.5% month-on-month. The PCE Core Deflator came in at 4.1% y/y/ vs. 4.2% expected. Earlier last week, we saw US GDP expanding by +2.4% in the second quarter, more than the +1.8% expected. We also had better-than-expected Jobless claims data.

Will it be a 25 or 50-bps hike for BoE?

Meanwhile, from the UK, we will have the Bank of England’s interest rate decision to look forward to on Thursday. The BoE is widely expected to raise rates by 25 basis points to 5.25%, although there is a risk of a repeat of June's surprise 50 bps hike—because UK inflation is much higher than it is in other big economies.

UK inflation came in weaker-than-expected last week, with CPI easing to 7.9% from 8.7% previous, core CPI falling to 6.9%, and other measures of inflation also declining across the board. Therefore, market chatter of a possible 50 basis point rate hike has been scaled back, which is why the cable has eased back down from its recent high of above 1.30. Nonetheless, a 25-bps hike to 5.25% is fully priced in, with markets expecting a further two rate hikes before year-end. But policy is now very restrictive, so will the BoE now signal a pause like the ECB did last week? If it does, then the pound could slump. Otherwise, the GBP/USD could hang around recent levels.

GBP/USD Technical Analysis

The GBP/USD has struggled to hold above the key 1.30 handle in recent weeks. Last week it nearly got there before being slammed down on Thursday, when it created a large bearish engulfing candle—the clearest signal yet that rates may have created at least a temporary top.

Following Thursday’s sell-off, the GBP/USD broke below a short-term bullish trend line that had been in place since early June, last week.

Source: TradingView.com

From here, it looks like the cable is poised to drop below Friday’s low at 1.2760ish. What it does thereafter may very well depend on the above macro events. Meanwhile, the clear invalidation point is now Thursday’s high at just shy of the 1.30 handle. If rates were to cross that level again, then the bearish bias would become completely invalidated. The bulls may therefore wish to wait for a clear bullish signal to form at lower levels or wait for an interim higher high to nullify the bearish signals we have had in the last couple of weeks.

To learn more about Fawad Razaqzada visit TradingCandles.com.