The stock breakout from last week is now consolidating just under 4,292...the level that designates a new bull market, states Steve Reitmeister of Reitmeister Total Return.

This is leading to some serious sector rotation that can often be quite confusing as you dig into the details. Thus, better to pull back to see the big picture, which is exactly what we will do in this week's Reitmeister Total Return commentary.

Market Commentary

First, let’s clarify why 4,292 is such an important level for stocks. That’s because the official definition of a new bull market is for the S&P 500 (SPX) to close 20% above the lowest closing price. As we go back to October 12, we find that the bottom was 3,577.03. Now add 20% to that equates to stocks needing to close above 4,292.44 to technically be called a new bull market.

Tuesday we ended at 4,283.85. Close...but no cigar. What has emerged this week is a consolidation period for the S&P just below this key level. Yet under the surface is the dramatic sector rotation. For example, on Monday small caps hit the matt after a strong uppercut to the chin. Then on Tuesday, they outperformed the large caps by 10X (not a typo).

What Does It Mean? Absolutely Nothing!

Consolidation periods are best appreciated as a “wait and see” period where investors are not ready to move higher...nor ready to pull back either. This has the overall market average barely moving daily. Yet between sectors and market cap groups, there can be large discrepancies between winners and losers.

The reason this type of action means nothing is that if you try and chase the sector rotation looking for trading wins you will almost always miss the action...like a dog chasing its tail. Just tired and confused. The better use of time for investors is to determine what happens after the consolidation period is over. As in, will we break higher confirming the new bull market or are we doing a serious correction?

There are two keys to predicting that outcome. First, what will the Fed do at their next meeting on 6/14? Second, what are the odds of a recession forming that would reawaken bearish sentiment? Let’s start with a discussion of the upcoming Fed meeting on Wednesday, June 14. Right now, investors see a 78% chance of no rate hike which matches up with many of the recent Fed official statements.

Before you cheer this as the highly anticipated pivot to more accommodative policies, then you should appreciate that investors expect a 51% likelihood of a 25-point hike at the July meeting. And another 11% expect that to be a bigger 50-point hike. Plain and simple, the Fed has been consistent about saying there is more work to do to get inflation down to the 2% target. And thus, you should not expect lower rates until 2024 to lower demand (aka slowing down the economy to slow down prices).

Please don’t forget that at the May meeting, Powell still pronounced that their base case pointed to a recession on the way before their job was done. I don’t think his tune will change at the June meeting which will likely throw cold water on bulls once again at the 6/14 announcement. Now let’s segue to the second topic that will weigh heavily on the market outlook. That being whether a recession is in the cards reawakening the bear from its recent hibernation.

Just roll back two paragraphs to appreciate that the Fed expects a recession before all is said and done with their rate hike regime. Next, consider this recession prediction I noted last week from famed Swiss money manager Felix Zulauf:

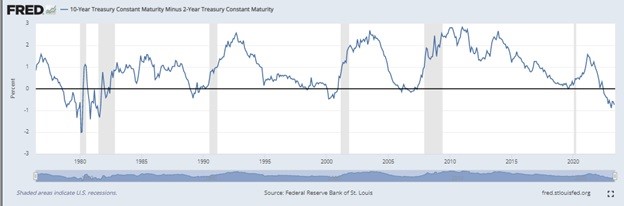

“We only know by hindsight when the recession started, but there is an indicator you can watch that gives you some indication when the start of the recession is here, without knowing for sure. And that is when the inverted yield curve begins to flatten.

“And, in the last few days or two weeks or so, we saw some flattening of that yield curve, and this could be an indication that we are very close to the beginning of a recession.”

And here is a correlated chart showing the two-year vs. ten-year rate inversion over time and its relation to recessions (gray bars):

Indeed, you can see that the recessionary periods did not happen at the deepest moments for the yield curve inversion. Instead, it took place after it flattens out and often starts to improve.

Now consider that as you look at the far right of the chart where the most recent inversion has started to flatten out. And correlate that with the 10% expected drop in corporate profits in Q2. And now correlate that to Fed expectations of a recession forming by the end of the year before they start lowering rates.

Third, consider the recent deterioration of some of the most widely followed economic indicators starting with ISM Manufacturing last Thursday. That was deeper in contraction territory at 46.9. For as bad as that sounds, the forward-looking New Orders component of 42.6 says things are likely to get worse.

But Reity, manufacturing is only 15-20% of the US economy. What are the readings from the much more meaningful ISM Services report? That tumbled from the previous positive reading to an anemic 50.3 showing with the employment component falling into contraction territory at 49.2. This means that service providers are getting more concerned about future growth prospects leading them to reduce their hiring plans.

If price action was your only guide, then yes there is some reason for excitement as we are on the border of a breakout into bull market territory. Yet when you appreciate the fundamentals, like focusing on Fed action and the current state of the economy, then it becomes harder to expect more upside at this time.

I suspect the consolidation period of just under 4,292 will extend til the Fed announcement on June 14. So please don’t get caught up in all the sector rotation nonsense until then. Better to prepare for what comes next. On that front, I predict that stocks will head lower in earnest starting the afternoon of June 14 as investors get reminded of the committee’s vigilant plans to squash inflation once and for all (which will likely squash the economy).

As they say “Don’t Fight the Fed”.

So, if they are telling you straight up that we will likely have a recession before all is said and done, then best to take them at their word. This means that stocks are more likely to go lower from here...and probably a lot lower.

Learn More About Reitmeister Total Return here…