The mighty early October bounce has already been wiped off the board as stocks tested new lows this week, states Steve Reitmeister of Reitmeister Total Return.

This is not a surprise to anyone whose head is not stuck in the sand as this bear market continues to unfold. We are at an interesting juncture where the fear of economic pain foretold by the Fed is not necessarily showing up in the economy. In fact, the current GDPNow reading for Q3 points to +2.9% growth. Now investors are in a "wait and see" mode for proof of that pain to appear in places like Q3 earnings season, which is about to roll out.

Let's discuss what the early earnings tea leaves tell us about what is in store this quarter. Also, I share insights on a nearly hidden topic no one is talking about yet...but foretells that this bear market may indeed last longer and fall further than many expect.

For now, the end of September lows are holding up without closing lower. That is likely because investors are awaiting the next catalyst. On the economic front that could come from changes in inflation or Fed policy. Here are the key dates to keep in mind:

10/12 = Producer Price Index (PPI)

10/13 = Consumer Price Index (CPI)

10/27 = Q3 GDP Price Index

11/2 = Fed Rate Decision

However, as the Fed told us, expect higher rates through end of 2023 as it is a long-term battle to get inflation down to size. Thus, don’t expect anything positive to come from these upcoming dates. Perhaps more essentially at this moment is what happens on the earnings front as we roll into Q3 reporting season. Even more important than the Q3 results is what they say about estimates for the future.

My old colleague, Nick Raich of EarningsScout.com, has some vital info to share on this front:

* We like to use the early 3Q 2022 reporters, companies reporting quarters ending in August, as a gauge on how overall earnings season will shape up when the majority report with quarters ending in September report this month.

* 20 S&P 500 companies have now reported their August quarter ends.

* Their next quarter (i.e. 4Q 2022) EPS estimate changes are the worst we have measured since the economy was being shut down for Covid in 2020.

* Steep cuts at CarMax, Carnival FedEx, Micron and Nike are the primary culprits for the negative revisions.

* We anticipate more negative revisions ahead based on these early reporters.

* Stay underweight stocks until we can determine when the worst of the cuts are over. There is a chance this earnings season will be the worst of the cuts. If so, the bottom in stocks will likely occur plus or minus three months from that point. Stay tuned.

The point being that more stars are aligned with stocks going lower. This brings us back to the important contemplation of determining bottom for this market. The short version is that somewhere around 3,000 is likely where bottom will be found. But that is the case if we use historical standards of the typical depths of bear markets.

But here is the rub...

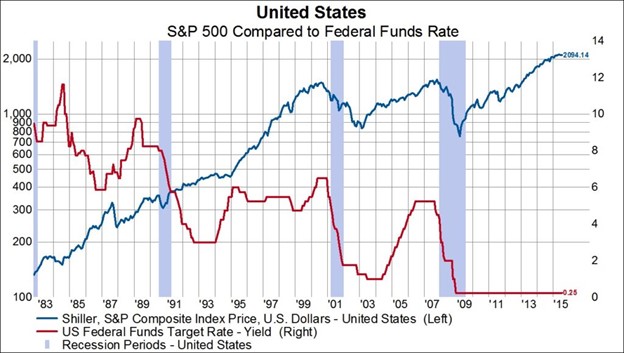

As we all know recessions and bear markets go hand in hand. So as the recession unfolds the Fed is actively lowering rates to help prop up the economy. This lowering of rates also makes cash and bonds less attractive leading more investors back to the stock market. This relationship shows up loud and clear in the chart below:

In general, the bear market bottoms as rates are plummeting lower. This is often what we call the TINA stock market environment where “There Is No Alternative” to owning stocks in the Fed induced low rate landscape.

Now let’s consider the current circumstances. Is the Fed lowering rates at this time as we sink into a bear market?

Heck NO!

Actually the Fed is raising rates at the most dramatic pace in history to help tame rampant inflation. In fact, the Fed is trying to CAUSE a recession to help lower demand, which leads to lower prices.

So as the recession unfolds, and as the stock market sinks lower, rates will NOT be low this time around. As you know they will be very high at this juncture and then the Fed will finally get around to cutting rates.

The point being that bottom for this market may be further out in time, and lower down in price, given this dynamic that rates are on the rise as the bear market unfolds. And thus, stocks will not be that attractive compared to 5-7% risk free rate on government bonds or 7-10% rates on high-quality corporate bonds.

Yes, it is a shade too early to contemplate all of this right now. But it is a fresh idea that came to mind that re-emphasizes why staying bearish is the right strategy.

And why our unique portfolio strategy continues to pay the bills like the +2.66% gain the past five sessions as the bear market sank to new lows.

Closing Comments

Obviously the above noted gains will turn to losses every time there is a bear market rally. However, as we look out over the short- to mid-term we appreciate why the market should head lower...and why our strategy should have us on the right side of market action.