Freeport-McMoRan (FCX) is highly dependent on the price of copper, the business cycle will continue to reflect slower growth, states George Dagnino, chairman of Peter Dag Strategic Money Management.

The decline in copper will have a negative impact on the price of FCX.

Freeport-McMoRan, Inc., engages in the mining of mineral properties in North America, South America, and Indonesia. The company primarily explores for copper, gold, molybdenum, silver, and other metals, as well as oil and gas.

The company also operates a portfolio of oil and gas properties primarily located in offshore California and the Gulf of Mexico. As of December 31, 2020, it operated approximately 165 wells.

Investors have not followed the money supply and its growth because inflation has not been a major issue from the late 1980s until recently. Growth in M2 has been close to 5%-6% on average in that period, thus accommodating solid economic growth with low inflation.

However, in the 1970s M2 growth has been rising well above its 5%-6% average. The outcome has been, then and now, rising inflation.

The main problem of rising inflation is it causes a decline in consumers’ spending power. It is no coincidence real disposable income has been declining since March 2021. Although retail sales are still growing at a rapid clip (+13.0% y/y), the impact of rising inflation is being felt in a major way.

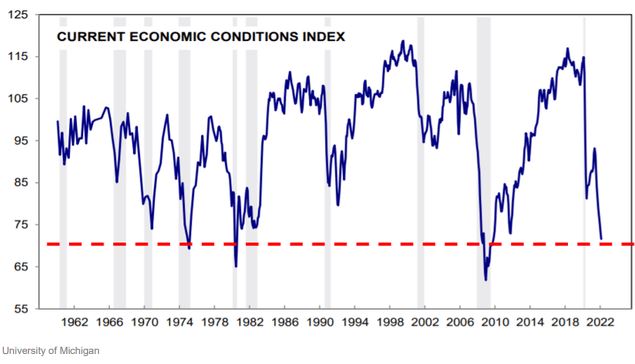

Consumer sentiment of the University of Michigan survey has declined to levels rarely seen in more than 60 years. Each time, it was associated with a recession.

The business cycles of the 1970s show an important pattern. Rising inflation is always followed by a recession, and the higher inflation goes, the more severe the recession is likely to be.

The Fed must slow down the growth of M2. They have no option if they want to tame inflation. Unfortunately, they are in a box.

The business cycle, meanwhile, is declining as the forces of recession keep rising. The likelihood of slower growth in demand and rapidly rising inventories will create imbalances, forcing business to slow down production. The inventory/sales ratio is already rising for wholesalers and overall business.

Slowing down production implies lower requirements for labor, commodities (such as copper, other metals, lumber, crude oil), and borrowing needed to improve or expand capacity.

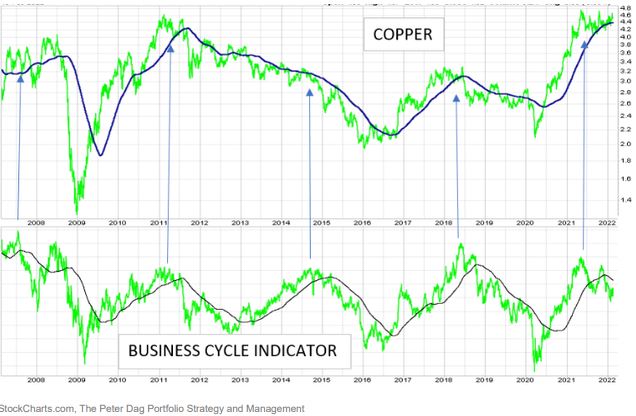

The above chart shows the price of copper in the upper panel and the business cycle indicator as published in real time from market data from The Peter Dag Portfolio Strategy and Management.

The decline in our business cycle indicator reflects a weakening economy. The graphs also show copper prices weaken when the business cycle indicator declines and rise when the business cycle indicator rises.

Right now, the business cycle indicator is declining and is likely to continue to decline as higher inflation keeps eroding consumers’ purchasing power and business is forced to reduce production to control inventories. The outcome is lower copper prices ahead.

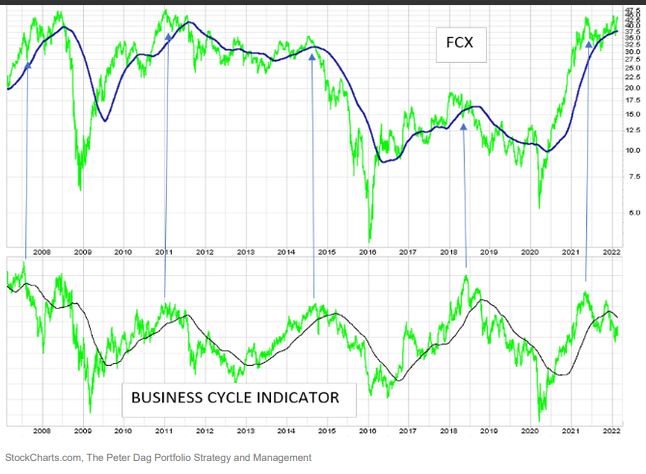

The above chart shows the prices of FCX in the upper panel. The lower panel shows the business cycle indicator. The weakness in the business cycle indicator points to lower prices for FCX.

Key takeaways:

- The rapid growth of M2—needed to finance Covid-19 stimulus programs—is fueling inflation.

- Inflation will continue to erode purchasing power, causing depressed levels in consumers’ sentiment.

- The slowdown in demand is already indicating inventories are rising too rapidly as reflected by the rising inventory/sales ratio.

- The needed inventory adjustment will cause production to slow down.

- The weakness in production will cause copper and other commodities to decline, making FCX unattractive.