With volatility rising, there are additional opportunities created trading the volatility instead of directions, says Dan Keegan.

This summer started out as a fairly, typical season of the lazy, hazy trading days of summer. Very little volatility was the rule of the day. The Cboe Volatility Index (VIX) dropped as markets hit all-time highs. Volume was light. Whether you were on the long or short end of premium, bleeding out profits was difficult. Let’s look at the time frame for SPDR S&P 500 ETF Trust (SPY) between July 15 and July 30. There was only one day where the intra-day range exceeded 1%, July 19th. The high was 300.07 and the low was 296.98.

That all changed on July 31, when the range was 295.20-301.20. The low for the ranges were in the 2% neighborhood with 3% being the norm. The combination of the prospect of slower rate decreases, an inverted yield curve and trade tensions led to a great deal of uncertainty in the markets. Trading options from the long side gives the trader tremendous leverage with a defined risk. Buying futures gives you greater leverage but as the trade goes against you, more money needs to be shoveled into it. That make carrying overnight positions difficult since the risk is not defined. Options, however, are a wasting asset. The time value that is embedded in the option premium is constantly eroding, and at an exponential rate.

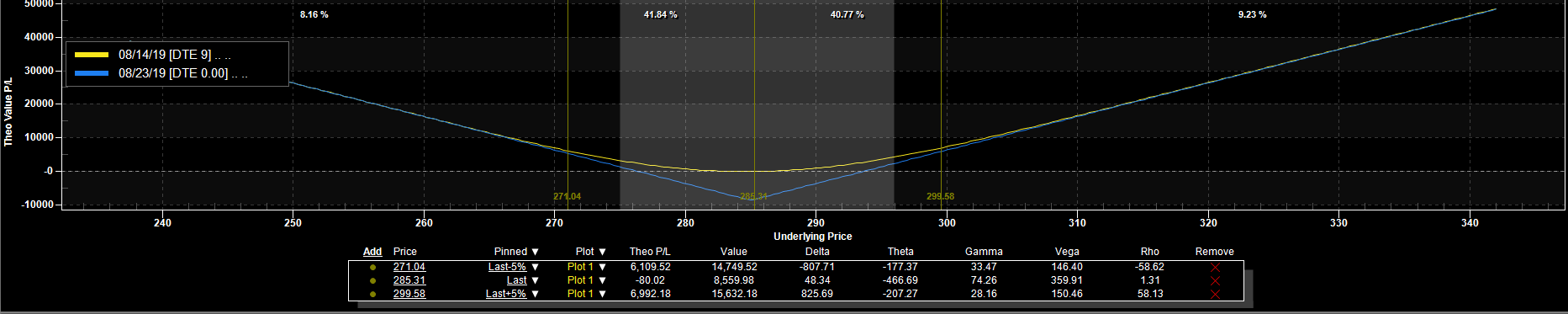

Let’s look at the SPY August 285 straddle that expires on the Aug. 23. With SPY trading at 285.00 the straddle can be purchased at 8.75. If left untouched, the upside breakeven point is 293.75 and the downside breakeven point is 276.25. The at the money straddle (292.50) closed last week at 6.44 (see chart).

Whenever there is increased movement, the price of leverage increases. Yesterday’s straddle is already in profitable territory with 7.5 trading days left. Does this mean that the SPY 285 straddle (expiring on the Friday Aug. 23) will be a loser if it stays within its range? No, it doesn’t. As SPY rises the calls pick up value and the puts lose value. The opposite occurs when SPY declines in value. You can hedge against your bullish position by selling shares of SPY. If SPY declines, you can buy back the shares for a profit (see chart). You can hedge against your bearish position by buying shares and then selling them out for a profit. The net, long options positions work well in a volatile environment.

You can reach Dan keegan at dan@optionthinker.com