Overall, our Global Risk Ladder leans risk on into the week ahead, but there are notable concerns with how expensive Technology (QQQ), Small-Caps (IWM) and the S&P 500 (SPY) present, writes Ziad Jasani.

My video commentary recorded June 18:

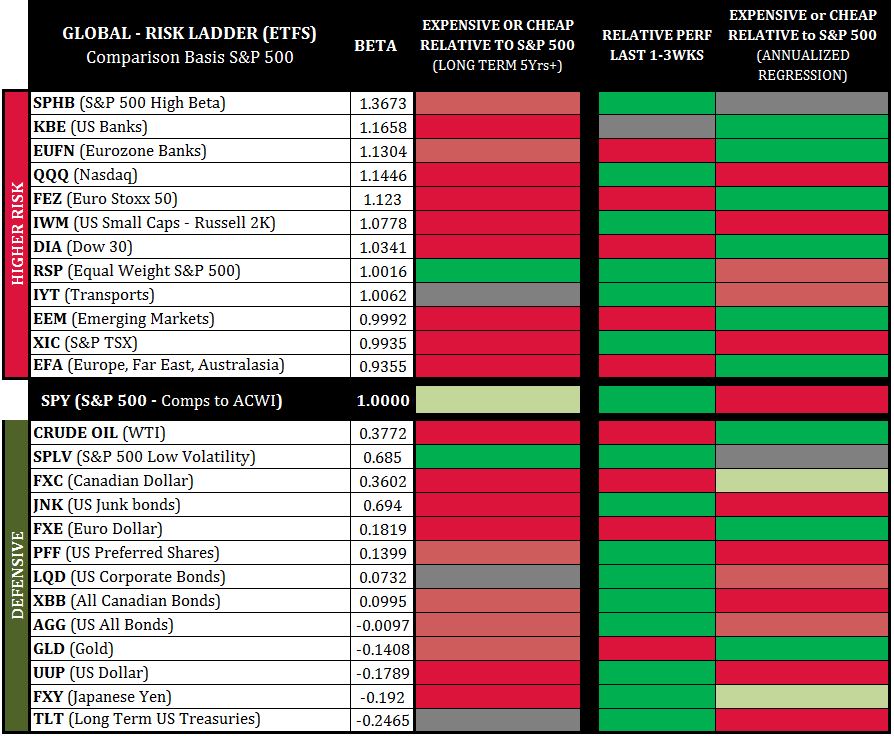

Global Risk Sentiment

Looking at the third column to the right we see a comparison of higher risk asset classes and defensive asset classes back to the S&P 500 (SPY) on an annual basis.

Comparison to the S&P 500 creates a “risk-ladder” where market risk is considered neutral.

When we see more green above the SPY line (middle line) and more red below we have a general “risk-on” signal; and vice-versa - red above, green below would be “risk-off.”

Currently, higher-risk asset classes are polarized.

Some very expensive some very cheap, indicative of the current geopolitical and tariff-trade-war issues (Cheap: Dow, Eurozone Financials, US Banks, Eurozone Stoxx 50, Emerging Markets, Eurozone Far-East & Australasia, Oil | Expensive: Nasdaq, Russell 2K, TSX, S&P 500).

Defensive Asset Classes largely present as very expensive, in particular the USD and Treasuries. For equities to advance, the USD must soften up.

This implies that any equity upside is likely short-lived (one week or at most two weeks before a move back down) or we have a few days of jitters (minor-risk-off) before risk-on presents.

View the Independent Investor Institute trading ideas and strategies videos here.