When we initiate a covered-call trade by first buying a stock and then selling a call option, our cost-basis, in the BCI methodology, is the lower of the stock price or strike price, explains Alan Ellman of The Blue Collar Investor.

If we sell an in-the-money (ITM) strike, we deduct the intrinsic-value component of the option premium from the share price bringing our cost-basis down to the ITM strike price. When we sell at-the-money (ATM) and out-of-the-money (OTM) strikes, the cost-basis is the stock price. This is all pretty straightforward but what if we have previously executed covered-call trades with this stock and retained it in our portfolio?

What if we decide to write calls on stocks we’ve held for long periods of time and are now at a much lower cost-basis than current market value? This article relates to an email sent to me in August 2020 from Stephen who was inquiring about his cost-basis as he continued to sell covered-call options on Bank of America Corporation (BAC).

Summary of Stephen’s Trades with BAC

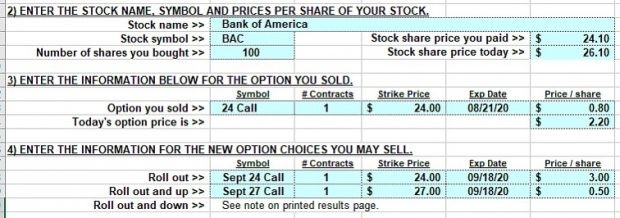

- Buy 100 shares of BAC at $24.10

- Current price $26.10

- Total per-share option premiums collected to date: $2.80

- Cost to buy back current $24.00 short call is $2.20

Stephen’s Dilemma

Stephen wanted to establish his cost-basis so as to make the best strike price selections. He was considering one of the following:

- $24.10

- $21.30 ($24.10 – $2.80)

- $26.10

Do Not Comingle Two Completely Different Sets of Calculations

We can view these trades through two sets of lenses: overall trade results and current trade situation. Are we evaluating where our series of trades stands as a final calculation or are we evaluating our trading decisions based on current information? If we wanted to evaluate our stock position with BAC to-date, our cost-basis has been lowered to $21.30…we paid $24.10 and received $2.80 in option premium.

If we were considering rolling the, now, ITM $24.00 call versus allowing assignment, we must ask ourselves what are our shares worth today? Prior to rolling the option, our shares are worth $24.00, our contract obligation to sell at the strike price. If we allowed assignment, that’s how much we would receive. To compare apples-to-apples, we must use $24.00 as our cost-basis, so none of the three choices Stephen was considering would be accurate for this specific purpose.

Calculating our Rolling Returns

Using $24.00 as our cost-basis and $2.20 as our cost-to-close the $24.00 call, Let’s use the What Now tab of the Ellman Calculator to see if the returns meet our one-month initial-time-value return goal range. Let’s assume the next month $24.00 call generates $3.00 and the $27.00 call generates $0.50.

Rolling Data Entry

BAC Data Entry into The Ellman Calculator

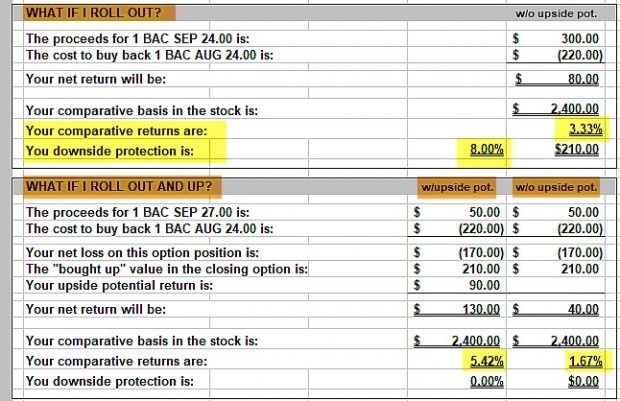

Rolling Calculations

BAC Rolling Calculation Results

Rolling-out results in a 3.33% initial time-value return with an 8.00% downside protection of that initial profit. Rolling out-and-up results in an initial time-value return of 1.67% but with upside share appreciation, a potential 5.42% one-month return if BAC moves up to the $27.00 strike by expiration.

Discussion

It is critical not to comingle two different sets of calculations when making our trading decisions. Our current trades should be based on current statistics while long-term evaluation of a series of trades will be based on longer-term data.

Learn more about Alan Ellman on the Blue Collar Investor Website.