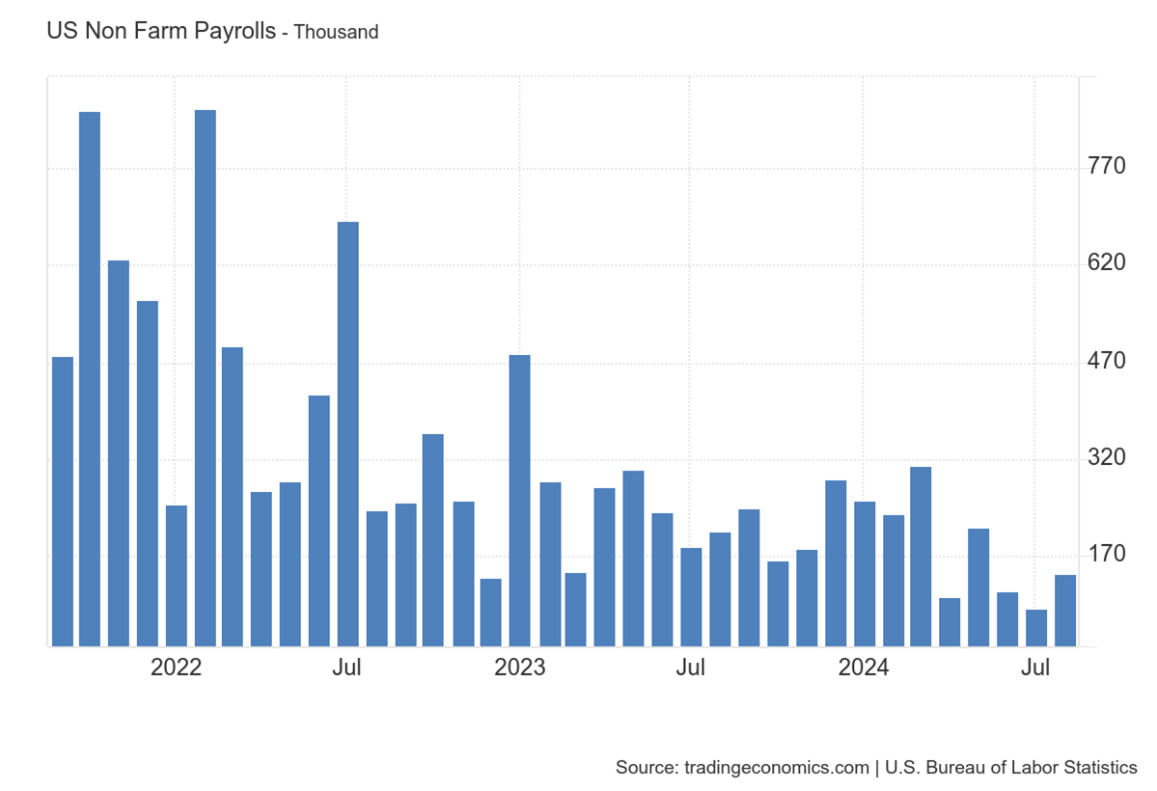

In the early going, equities are off their morning lows. Most other markets are gyrating wildly. Why? It all stems from this morning’s August jobs data.

Economists were expecting a gain of 160,000 jobs in August, along with an unemployment rate reading of 4.2%. Average hourly earnings were forecast to rise 0.3%. The report showed the US economy ACTUALLY created only 142,000 jobs last month. PLUS, the July and June figures were revised down by a combined 86,000. That’s a whopper of a reduction. Unemployment was in-line at 4.2% while earnings rose a slightly higher-than-expected 0.4%.

Non-Farm Payroll Change (Monthly, 3-Year Chart)

What does it all MEAN? Interest rate markets (and market pundits!) have been all over the map in 2024 when it comes to Federal Reserve policy expectations. They were pricing in six-to-seven cuts in 2024 at the start of the year...then essentially NO cuts back in May.

More recently, they have been primed for around 75-100 basis points in cuts through year end – and in the wake of the data, those projections are RISING. In other words, markets are INCREASING bets on a 50-point cut at the meeting that concludes Sept. 18. I think that interpretation is CORRECT. In fact, I have been saying for weeks that is the RIGHT move for the Fed to make. It has two more scheduled meetings after September, one each in November and December.

In other news: Investor sentiment has been shaky in the semiconductor space for several weeks now – and chipmaker Broadcom Inc. (AVGO) didn’t do the sector any favors. The firm beat fiscal Q3 sales and earnings estimates. But its Q4 revenue forecast was a bit light.

Broadcom sells chips into a wide range of end markets, including data centers, automobiles, and mobile devices. But while AI-driven demand is strong, non-AI demand is coming in somewhat weaker. The stock tumbled, eroding the hefty year-to-date gains it had previously racked up.