Magic Software Enterprises Ltd. (MGIC) isn’t a household name even in the tech world — but that’s never been the point. For over three decades, this Israel-based company has quietly played a pivotal role in enterprise digital transformation, notes George Gilder, editor of Gilder’s Technology Report.

It provides behind-the-scenes tools and services that keep large organizations running efficiently: Application development platforms, business process integration, IT consulting, and outsourcing. Magic is the connective tissue that helps modern enterprises integrate legacy systems, streamline operations, and adopt new technologies without tearing everything down.

Now, Magic is undergoing a transformation of its own — one that could alter its trajectory for years to come. It recently announced a plan to merge with Matrix IT, Israel’s largest IT services firm. That move indicates a shift from incrementalism to something more ambitious.

The companies have signed a Memorandum of Understanding that, if finalized, will see Magic become a wholly owned subsidiary of Matrix, with shareholders receiving Matrix stock in return. The proposed deal would value the combined entity at $2.1 billion.

The merger has clear logic. Magic brings a strong international footprint—particularly in North America and Europe—along with its proprietary low-code/no-code development platforms and a portfolio of packaged software solutions. Matrix is deeply embedded in the Israeli market, executing many of the country’s largest IT projects and representing an extensive range of software vendors.

Together, the companies would operate in approximately 50 countries and serve more than 6,000 clients, supported by a combined workforce of 15,000 employees.

For current shareholders, the proposed merger offers both upside and uncertainty. The deal structure—where Magic shareholders receive Matrix stock based on a 31.1% / 68.9% split — was approved by an independent committee and reflects a thoughtful valuation process, especially given the shared controlling shareholder (Formula Systems). The transaction is expected to be accounted for using the pooling-of-interests method, avoiding goodwill amortization, and preserving balance sheet clarity.

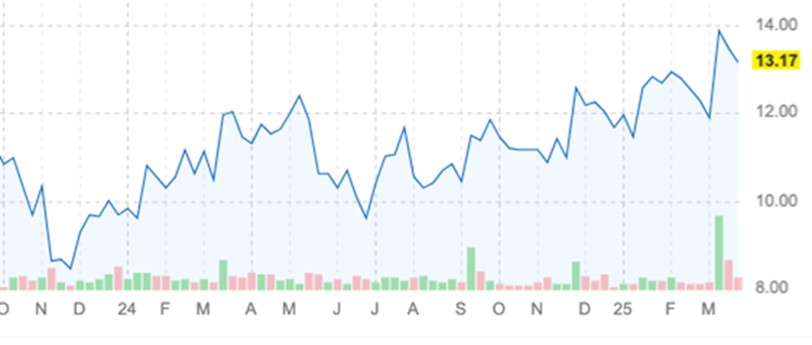

A successful merger will require deeper valuation work, especially as the deal terms take shape. But with Magic still trading at a forward P/E of 11.5 — roughly half that of the Russell 2000 — it remains attractively priced for long-term investors. This isn’t a momentum play, but in a portfolio built around solid compounders with breakout potential, Magic continues to earn its place.