One of my more successful warnings to investors and subscribers over the past couple years has been the reverse yen carry trade. Now, it’s happening again – and impacting the S&P 500 (SPX), writes Michael Gayed, editor of The Lead-Lag Report.

A brief refresher: For years, traders and institutions have borrowed cheap yen at 0% or near-0% interest rates in order to put the proceeds into higher returning assets, namely US tech stocks and the dollar. That trade works as long as borrowing rates remain ultra-cheap.

The problem today is that those borrowing costs are starting to get more expensive. Traders who were able to access virtually free capital for years are now finding themselves sitting on costly margin positions that they’re potentially being forced to unwind. That forces people to sell dollar-denominated assets, which raises volatility and sends risk asset prices lower in the process.

This most famously happened in August of last year. After the Bank of Japan raised rates by a quarter-point earlier in 2024, they caught the markets off guard with a second hike not long after. That triggered a huge rally in the yen that at one point drove the VIX above the 60 level and ignited a roughly 10% correction in the S&P 500

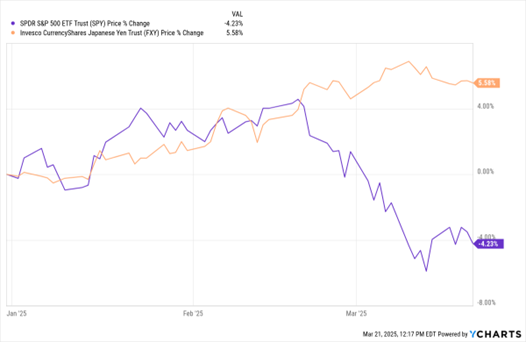

FXY Vs. SPY (YTD % change)

Data by YCharts

If you look at what conditions were like during the original yen carry trade and what they are now, you’ll see that they’re not all that different. The yen is strengthening again (Editor’s Note: See the Invesco CurrencyShares Japanese Yen Trust (FXY) in the chart above). Long-term Japanese bond yields are moving steadily higher. The Bank of Japan is still trending towards moving rates higher over the next 12 months...while the Fed is likely going to be able to move rates lower at some point over the next 12 months.

This is the same forward-looking view that existed prior to the last carry trade reversal. Whether the market realizes it or not (and with all of the attention right now going to tariffs and foreign trade policy, it may not), the second reverse yen carry trade is already in process. It’s just happening much slower this time around.

Because it’s happening slowly and steadily instead of sharply and suddenly, it hasn’t been getting nearly the same attention. With geopolitics and a global trade war dominating the market narrative, investors are missing the damage this is doing to markets – and the risk that they’re still being exposed to.

In short: Japan is still the real risk.