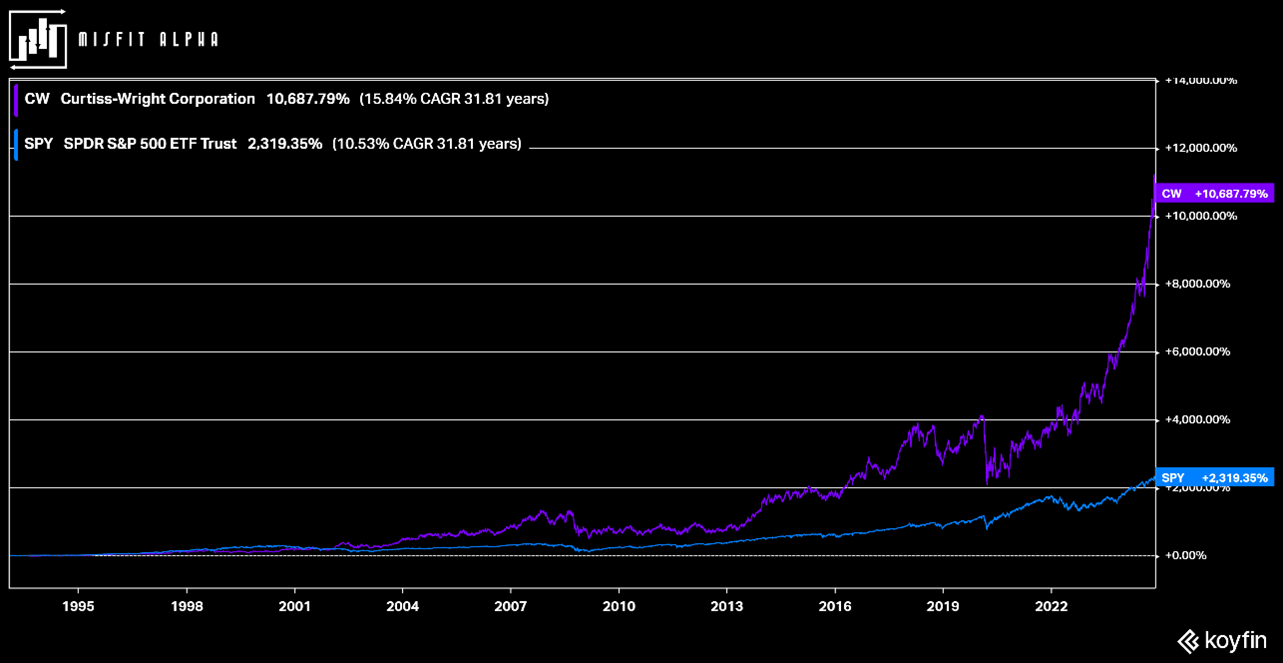

Nuclear energy appears to be having its time in the sun. Many large tech companies and AI investors think nuclear energy is uniquely positioned to power data centers. I like a company that supplies equipment to every active nuclear power installation in the US (civilian and military): Curtiss-Wright Corp. (CW), explains Tyler Crowe, editor of Misfit Alpha.

The future of nuclear power is in tension, though. The most recent nuclear reactor built in the US was billions over budget and years behind schedule, and the contractor building it filed for bankruptcy during the process.

One alternative solution is the development of new reactors. There are many options: Small modular reactors, transportable microreactors, fluoride salt-cooled reactors, light water reactors, and molten chloride reactors. Pretty much everything is on the table these days.

Which brings me to CW. Most people don’t look at Curtiss-Wright as the gatekeeper to America’s nuclear industry. Maybe that’s because it’s embedded within a diversified industrial manufacturer and defense contractor, or maybe it's because few Wall Street analysts or the investing media cover it. Whatever the reason, it fits many of the traits of a Misfit stock.

The most intriguing aspect of the business, at least for this exercise, is its Naval and Power division. It’s the primary supplier of nuclear propulsion systems and equipment for the US Navy. About 56% of its revenue comes from defense contracts.

This division is also one of the largest suppliers of nuclear reactor components in North America. Curtiss-Wright components are in every operating reactor in North America. It also has an exclusive supply and maintenance agreement with Westinghouse Electric for its AP1000 nuclear reactor.

As of this writing, there are 13 AP1000s in operation globally with another 19 under construction. The AP1000 is the design used for the most recent nuclear plant in the US, Southern Cos.’ (SO) Vogtle plant in Georgia.

Curtiss-Wright falls squarely in the basket of a company that will get overlooked by many investors for many reasons. It also likely doesn’t pass many investors’ stock screens. Revenue growth over the past decade has been tepid, its net income margins and returns on invested capital are in the low double digits, and its low yield dividend (0.23%) and slow dividend growth (5% annually over the past 10 years) aren’t often the kind of performance numbers that get investors to jump out of bed and hit the "Buy" button.

But the fervor about nuclear isn’t about the current industry. It’s about the future, with demand growing significantly. On that front, things look much more promising. Curtiss-Wright’s management projects its commercial nuclear business will double revenue by the end of 2028.