We've been less dovish on interest rates than the markets since mid-June because we've been more bullish on the economy and the labor market than the consensus. And last week’s economic releases showed the US economy continues to chug along, notes Ed Yardeni, editor of Yardeni QuickTakes.

The services-providing sector remains strong, and there are even green shoots sprouting in housing. Abroad, there's some optimism percolating that real growth may be improving in Europe. Nevertheless, we continue to favor the US over the Eurozone. The US has a much more compelling growth story, in our opinion.

(Editor’s Note: Ed Yardeni is speaking at the 2024 MoneyShow Orlando, which runs Oct. 17-19. Click HERE to register.)

Here's more:

(1) Purchasing Managers Surveys. The August flash PMI report from S&P Global for the US showed that the NM-PMI rose from 55.0 in July to 55.2 in August, while the M-PMI fell from 49.6 to 48.0. Prices charged for goods and services rose at their second-slowest pace since June 2020. This all aligns with our view that the services economy's strength is still offsetting the rolling recession in goods, and that disinflation prevails.

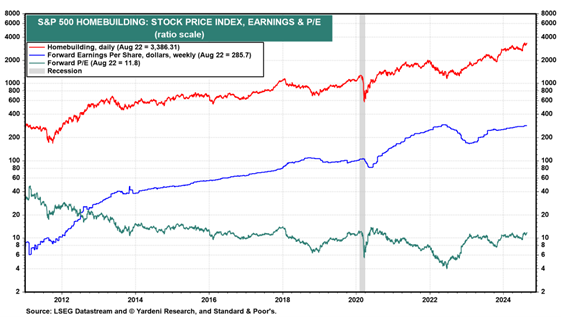

(2) Housing. July's existing home sales rose 1.3% month-over-month to an annual rate of 3.95 million units, stronger than expected. Sales were down 2.5% year-over-year. But with the average rate on a new 30-year fixed-rate mortgage down to 6.49% from a six-month high of 7.22%, we expect that housing will recover from its rolling recession in coming months. Indeed, the S&P 500 Homebuilding stock price index is back in record high territory (chart below).

(3) Europe. Flash NM-PMIs for the Eurozone were stronger-than-expected, perhaps indicating growth is recovering in the region. However, much of the Eurozone's strength came from France, where the NM-PMI jumped from 50.1 to 55.0 thanks to hosting the Olympics. The region's M-PMI remained depressed in August.

Another potential positive was that negotiated wage growth fell from 4.74% YOY in Q1 to 3.55% in Q2. Perhaps that gives the European Central Bank room to cut rates a bit quicker.