Even following the late-month selloff, stocks entered the final trading week of July barely changed for the month. August has been volatile so far, with the stock market reacting to weak economic data from the industrial and jobs economy and concerns that the Fed has remained restrictive for too long. But given its strong first half, the stock market is still up year to date, notes John Eade, president of Argus Research.

Recent turmoil is consistent with ongoing uncertainty. The nature of the presidential election changed dramatically over the past month. The Fed also appears to be teeing up 50 basis points or possibly even 75 bps of interest rate cuts by year end. No cuts appear likely until mid-September, though, leaving investors and consumers dangling.

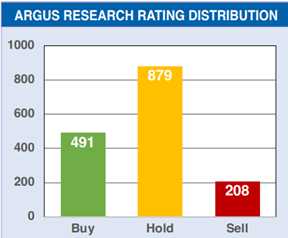

Amid the uncertainty, the second-quarter earnings season has been a bright spot. While good past-quarter earnings are always important, investors hold their breath regarding current-quarter outlooks. Companies generally reaffirmed the moderately positive outlook for the full year, which is still trending toward high-single-digit to low-double-digit EPS growth for 2024.

While the S&P 500 was little changed in July, significant sector realignment took place. The iShares US Technology ETF (IYW) was down 5% for the month and the Communication Services Select Sector SPDR Fund (XLC) was down just under 2%.

Where did the money go? Lots flowed into the iShares US Financials ETF (IYF), which was up 6% for the month. Upcoming cuts in the fed funds rate can be expected to pinch banks’ net interest margins. But 2Q24 earnings season for the sector has been highly positive, featuring recovery in fee-based businesses such as investment banking. Upcoming lower interest rates can also be expected to rekindle loan and mortgage growth.

Other winning sectors in July included the iShares US Utilities ETF (IDU), up 7%; the iShares US Industrial ETF (IYJ), up 5%; Healthcare, up 4%; Consumer Staples, up 2%; and Materials, up 2%. Most of these rose with the market early in the month and were able to hold on to gains on generally positive second-quarter earnings results.

Large-cap Information Technology and Communication Services stocks were in rally mode for all of 2023 and the first half of 2024. But the market has not been kind to large technology companies reporting anything less than stellar earnings for the second quarter. The current rotation away from AI champions and toward defensive and cyclical sectors may have room to run.

Meanwhile, July nonfarm payrolls of 118,000 badly missed the consensus estimate of 175,000. The bigger focus was on the unemployment rate, which shot up to 4.3% in July from 4.1% in June. That triggered the Sahm indicator, which says that when unemployment rises 50 bps within a cycle, recession follows or has already started.

US GDP grew 2.8% in 2Q24, and Fed Chairman Powell has called the Sahm indicator a “statistical regularity” rather than an economic rule. Nonetheless, investors are now more nervous about recession than they have been since the pandemic days. Interest rates across the Treasury yield curve have moved sharply lower, and the likelihood of more-aggressive Fed action appears to be rising.