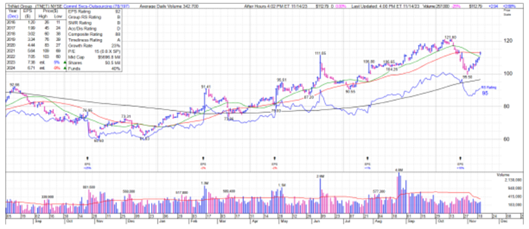

TriNet Group (TNET) is a $5.7 billion company offering outsourced Human Capital Management (HCM) solutions to the fragmented small- and mid-sized businesses market. This is an interesting trade opportunity in a little-known stock that’s doing well even though revenue is likely to be down both this year and next (EPS should grow this year), remarks Tyler Laundon, editor of Cabot Small-Cap Confidential.

What’s the story? Well, it’s a strong employment market in some areas, but not tech, which is where TriNet has a good amount of exposure. Still, with high post-pandemic regulatory complexity and dispersed workforces, employers are continuously tasked with pressure to provide competitive salaries and benefits to attract and retain talent.

That’s not always easy for smaller players, which is why many turn to services like QuickBooks from Intuit (INTU). TriNet offers a compelling alternative.

Solutions are sold under the professional employer organization (PEO) model, which means TriNet acts as the employer of record for admin and regulatory purposes for worksite employees. This co-employment model means businesses get a high-touch employee benefit provider that operates at scale, handles day-to-day HR functions, and has competitive employee benefits, while also sharing employment risk liability.

For its part, TriNet is careful about the risk profile of clients that it takes on given that it has an at-risk insurance model. It focuses on high-growth markets that include tech, financial services, life science, non-profit, and professional services.

The company reports in two segments with insurance services (workers comp, actuarial expertise, health insurance) generating the bulk of revenue (85% in 2022) and professional services generating the remaining 15%.

The company’s main competitor is Automatic Data Processing (ADP). Not surprisingly, both flagged lower tech hiring in Q3 and shares of ADP were whacked while TNET was flat, probably because the company did well in health care.

On the conference call, TriNet management was upbeat and suggested that Q4 trends were okay and that insurance risk has been very well managed (i.e. low claims payouts). It seems like salespeople are doing a bang-up job, even in a soft tech market. And while there’s no tech hiring boom on the immediate horizon, decent win rates, a $1 billion share repurchase program, and a discounted valuation have investors snapping up shares of TNET.

It’s not a stock I want to get into a long-term relationship with right now. But it looks like an interesting momentum play. We’ll take a swing.

Recommended Action: Buy TNET.