Famed investor Warren Buffett coined one of my favorite quotes: “Price is what you pay, value is what you get.” Buffet was referring to buying stocks, but we all apply this simple advice to everyday life choices. Many consumers are now turning to private-label merchandise to save money, and Target Corp. (TGT) is a key beneficiary, explains Kelly Green, editor of Dividend Digest.

As consumers find themselves staring down the barrels of inflation and shrinkflation (less product for the same price), this balance of price versus value is playing a greater role in buying decisions. One popular solution is to buy private-label or store brands in place of name brands. CNET notes that, on average, you can save about 40% by buying store-brands rather than their name-brand equivalents.

Consumers must be finding value as store-brand sales account for around 21% of the $1.7 trillion annual grocery industry. The Private Label Manufacturers Association recently reported that store-brand sales jumped 8.2% during the first half of 2023.

Retailers, in general, have been catering to this growing market with the creation of private brands at various price points. Walmart (WMT) has Great Value, Equate, Sam’s Choice, and Member’s Mark. Costco Wholesale (COST) has Kirkland. BJ’s Wholesale Club (BJ) has Wellsley Farms.

As for Target, it has over 45 private label brands, which they call “owned brands.” You can find them in every department of the store and at every price point. Many shoppers don’t realize that these are Target-owned brands—but they’re in millions of kitchen pantries.

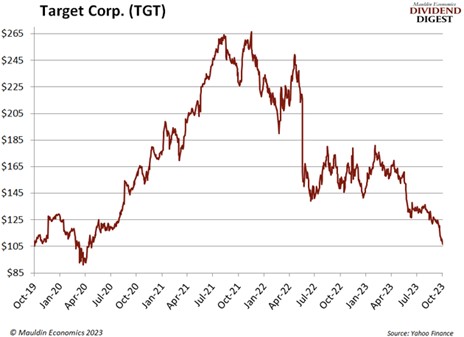

Target has been the subject of ideological debate over the past year. The dispute has polarized the brand among its patrons and clobbered the share price, down 37% from its 2023 high. I don’t shop at Target, but when I see an opportunity to earn a 4.1% yield from a giant retailer, it deserves a closer look.

Target is a Dividend King, having raised its dividend every year for the past 54 years. During the pandemic, Target had some amazingly profitable quarters. It was a unique period that enabled Target to hand above-average annual dividend increases to its shareholders. Added bonus: Shares have slid all the way back to early 2020 levels.

That combination now gives us a post-COVID dividend at a pre-COVID price—and potentially a great deal.

In Target’s last earnings call, the company acknowledged it faces a few challenges. Management also lowered its full-year earnings per share to a range of $7.00–$8.00, down from its previous guidance of $7.75–$8.75. Even if earnings are at the bottom of the range, the dividend will be more than covered… with room for some growth.

Recommended Action: Buy TGT.