Energy stocks have generally trended lower, with the S&P Energy Index recently underwater by around 10% year-to-date. But that means several energy stocks now trade below their “Dream Buy” levels, including one I really like, Kinder Morgan Inc. (KMI), writes Elliott Gue, editor of Energy and Income Advisor.

The selling of energy stocks has become largely indiscriminate. That’s normal when the overall stock market starts to roll over. And the turmoil in the banking sector has provided a good reason for investors to trim their holdings of stocks, including industries that are firmly in long-term up cycles like oil and gas. So long as that’s the case, we’re going to play things cautiously.

But what’s behind the long-term energy cycle is years of under-investment in new supplies and infrastructure. The Federal Reserve’s rate hikes, combined with falling oil and gas prices, have if anything made that situation a good deal worse by further discouraging investment in supply.

That means when demand does return there will be an even worse supply gap, which will push up energy prices and energy stocks to new heights. Energy markets are still in the very early innings of the up cycle.

As for KMI, “Dream Buy” prices represent levels of valuation where our stocks in the past have traded only under extreme circumstances. An example would be the pandemic market crash in 2020. Buying them at these levels has never failed to produce windfall profits for patient investors.

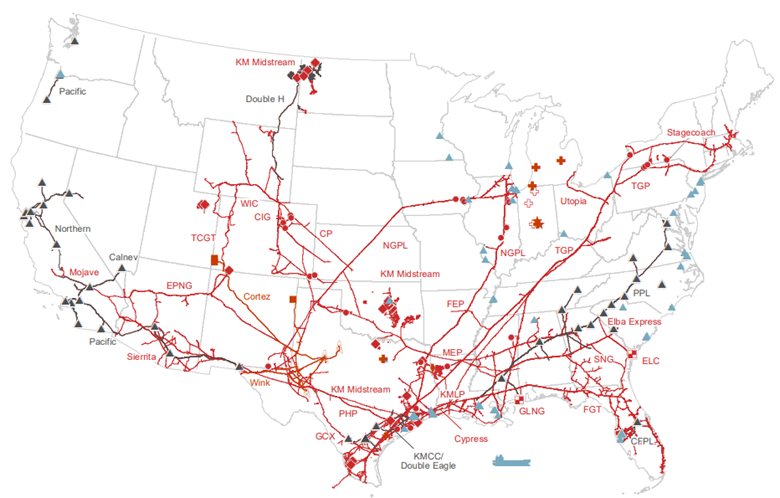

Kinder Morgan (KMI) Asset Map

All of Kinder’s ongoing midstream projects are reportedly on time and on budget. The company also no longer has the exposure to variable rate debt that it did last year, which should ensure it meets management’s flat guidance for 2023 distributable cash flow and EBITDA.

Kinder does face an uncertain outcome in a federal court challenge to a Federal Energy Regulatory Commission permit for its East 300 natural gas pipeline. If the court rejects the permit and forces additional filings, it could add considerably to the final cost.

But most observers rate Kinder’s odds of victory as very good. Even if it’s defeated, guidance would be unlikely to change much, with the company easily generating free cash flow in excess of dividends to keep whittling away at its debt.

Recommended Action: Buy KMI up to $22.