The dominating narrative right now remains the 3-pronged scenario of high inflation, ongoing supply chain disruptions, and the threat of recession, asserts Peter Krauth, commodity sector expert and editor of Gold Resource Investor.

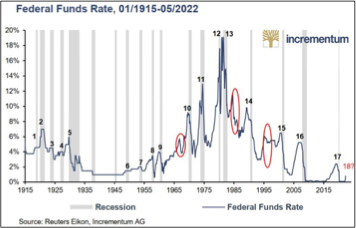

At this point, it would surprise me if the Fed managed to pull off a “soft landing”. That’s when interest rates are raised just enough to sidestep the economy overheating (from inflation) and avoiding a recession.

Let’s be clear. The odds of avoiding a recession are very low. It almost never happens once the Fed starts a rate-hiking cycle. The Fed knows this, but they continue to pretend otherwise.

And yet, history tells us very clearly that, since the Fed was created in 1913, it has raised rates 20 times. Indeed, only three of those times did the Fed manage to avoid a recession.

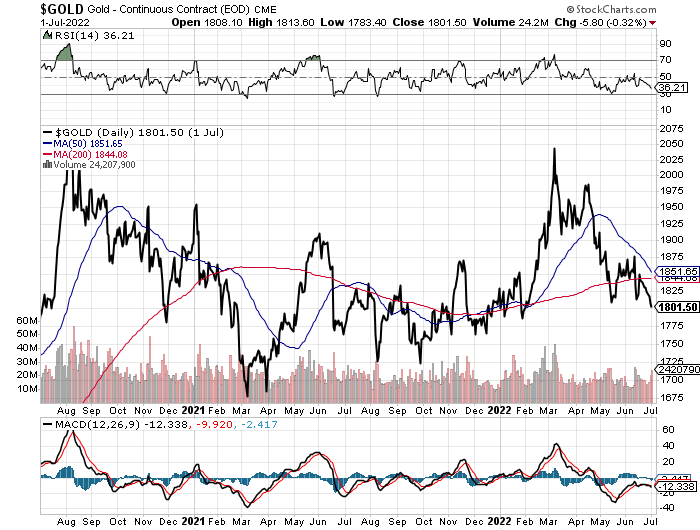

Gold has managed to hold quite steady near the $1,800 mark, nearly flat since the start of the year and dramatically outperforming stocks and bonds. In my view, central bank buying has been a major driver.

The annual central bank survey by the World Gold Council shows that participants continue to view gold favorably as a reserve asset. In fact, 25% of respondents confirmed they have plans to increase their gold reserves, up from 21% last year.

Central bankers know they should raise rates considerably to fight inflation. But the reality is their hands are tied. Debts are enormous, higher rates would crush the economy and dramatically weigh on over-indebted governments, businesses, homeowners, car owners and student debtors. My point is, the rate-hiking cycle will not get very far.

So, while we may face ongoing headwinds for commodities in the near term, I expect precious metals and resources will perform well under the new paradigm.

Meanwhile, gold seems to be testing about the midpoint of the last triangle. The RSI and MACD suggest ongoing negative sentiment, with room for the RSI to bottom at/near 30. So, I think we could see a retest of the $1,775 level, which has shown previous support, before a final bottom is in.

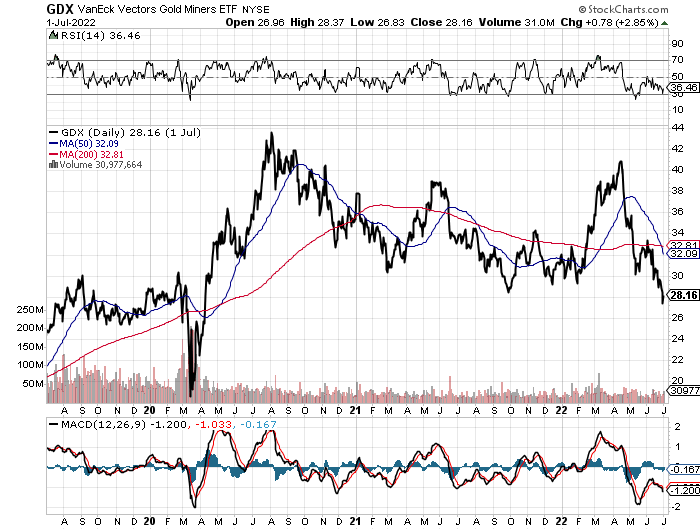

Now looking at gold stocks, it seems we may be approaching a low. The VanEck Vectors Gold Miners ETF (GDX) has broken a multi-year low just above $28. The RSI momentum indicator may need to trough a bit lower, while the MACD is looking quite washed out already.

SSR Mining (SSRM) announced it was being included in the Russell 1000 Index, as well as the broad-market Russell 3000 Index. These indices are widely used by investment managers and institutional investors for index funds and for active investment strategies.

This development is likely to lead to more buying of SSR Mining as investors look to track these indices. SSRM — which has operations in the US and Canada as well as Argentina and Turkey — has held up better than its peers but is also oversold. The shares are attractive to accumulate on weakness.

Alamos Gold (AGI) announced initial production from its La Yaqui Grande mine (Sonora, Mexico), ahead of schedule. La Yaqui Grande is one more discovery that helps extend the life at the Mulatos Complex which began in 2005.

Higher grades and recoveries at La Yaqui will help drive higher output and lower costs, leading to improved cash flow in H2 this year and onward. Alamos has become quite oversold and is attractive to accumulate.

Sibanye Stillwater (SBSW) reported that its US platinum group metals operations were largely unaffected by widespread damage to infrastructure and personal property in Montana, USA. However, with several nearby bridges affected, operations are being suspended for about 4-6 weeks so that safe access and production can resume.

SBSW will also be increasing it ownership in Keliber Oy — a Finnish mining and battery chemical company. SBSW has sold off considerably along with most of the commodities sector. The shares are attractive to accumulate on weakness.