Are valuations still a concern given the strong economic rebound and earnings growth? asks Jim Stack, a leading "safety-first" money manager and editor of InvesTech Research.

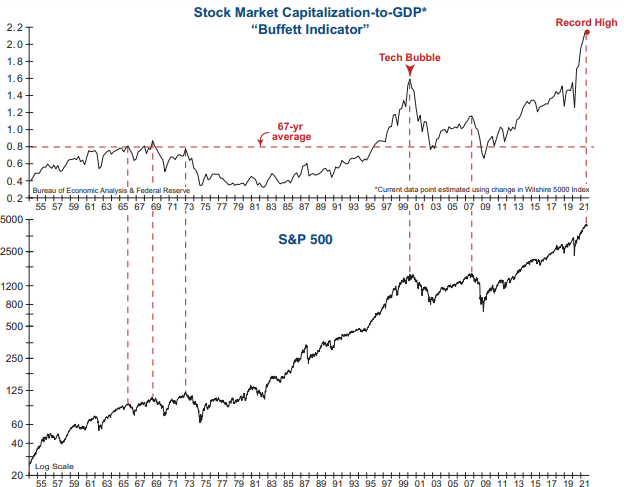

The short as well as the long answer is yes — valuations are still a major concern! And nowhere is today’s valuation problem more evident than in Warren Buffett’s preferred equity market valuation tool, the Stock Market Capitalization- to-GDP ratio.

Also known as the “Buffett Indicator,” this valuation metric has surged well beyond its previous all-time high from the Tech Bubble — thanks to trillions of dollars in monetary and fiscal stimulus since the onset of the pandemic.

When valuations reach historic extremes, or even extremes relative to recent years, the risk of a bear market can rise dramatically (vertical lines on graph).

While some believe that the current high valuations will be resolved by robust economic growth, history suggests that’s not realistic. With the economic recovery in full swing, nominal GDP grew at an annual rate of approximately +13% last quarter, yet the Buffett indicator is still at an all-time high.

Furthermore, economic growth cannot sustain that hectic pace going forward. Consequently, the extreme reading in the Buffett Indicator is unlikely to quietly disappear without a major bear market.

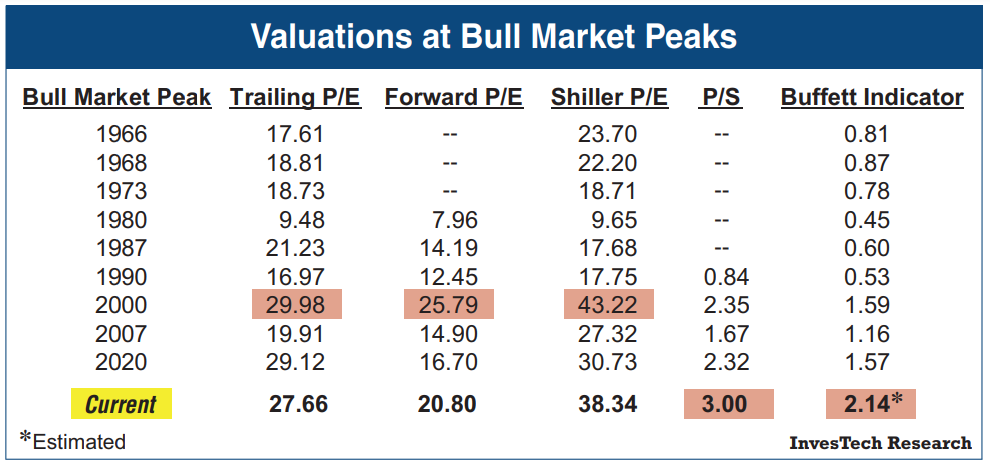

Today’s valuation problem extends beyond just the Buffett Indicator. As shown in the table below, the stock market is more expensive today than at nearly every market peak in the past 60 years, regardless of the valuation measure.

Despite the earnings-based valuation ratios easing slightly from when we last published this table in July, all the current readings of the featured valuation metrics remain above the 90th percentile on a historical basis.

In short, no matter which valuation measure you choose, equities are extraordinarily expensive relative to history even when considering the strong GDP and earnings growth experienced thus far in 2021.

While high valuations are not an effective timing tool, they do reflect an investor’s level of risk. And current valuations suggest investors still have very little margin of safety today.